How to buy carbon credits that deliver real impact

Offsetting is a critical part of the net zero equation – but it remains a challenging and often opaque process.

This blog outlines the role detailed due diligence can play in finding high quality credits.

Following the mitigation hierarchy, businesses should prioritise avoiding and reducing emissions. The Voluntary Carbon Market (VCM) can however play a vital role in mitigating the impacts of residual emissions that we cannot immediately reduce.

By investing in carbon credits now, rather than waiting, businesses can accelerate their climate action, support global carbon reduction projects, and demonstrate leadership in the transition to a low-carbon economy.

Poor-quality carbon credits undermine the credibility of the entire market, and what it is trying to achieve for both businesses and project beneficiaries.

Unfortunately, there has been much negative focus on voluntary carbon markets, which are sadly beset with examples of cheap, poor-quality credits that fail to deliver their promised impact.

It is clear that within the VCM the effectiveness of carbon credits is highly dependent on their quality. However, this does not diminish their importance in the net zero equation – when done right.

A high-quality credit ensures that a project delivers real and measurable carbon impact as well as broader environmental and social co-benefits.

Buying credits is a challenging, often opaque process. While there are organisations like The Integrity Council for the Voluntary Carbon Market and The University of Oxford’s Oxford Offsetting Principles working to improve robustness of the market, businesses still need to take responsibility for understanding and de-risking their carbon credit portfolio.

Strong due diligence is essential to ensure that carbon credits not only contribute meaningfully to the reduction of greenhouse gases but also uphold the highest standards of environmental integrity.

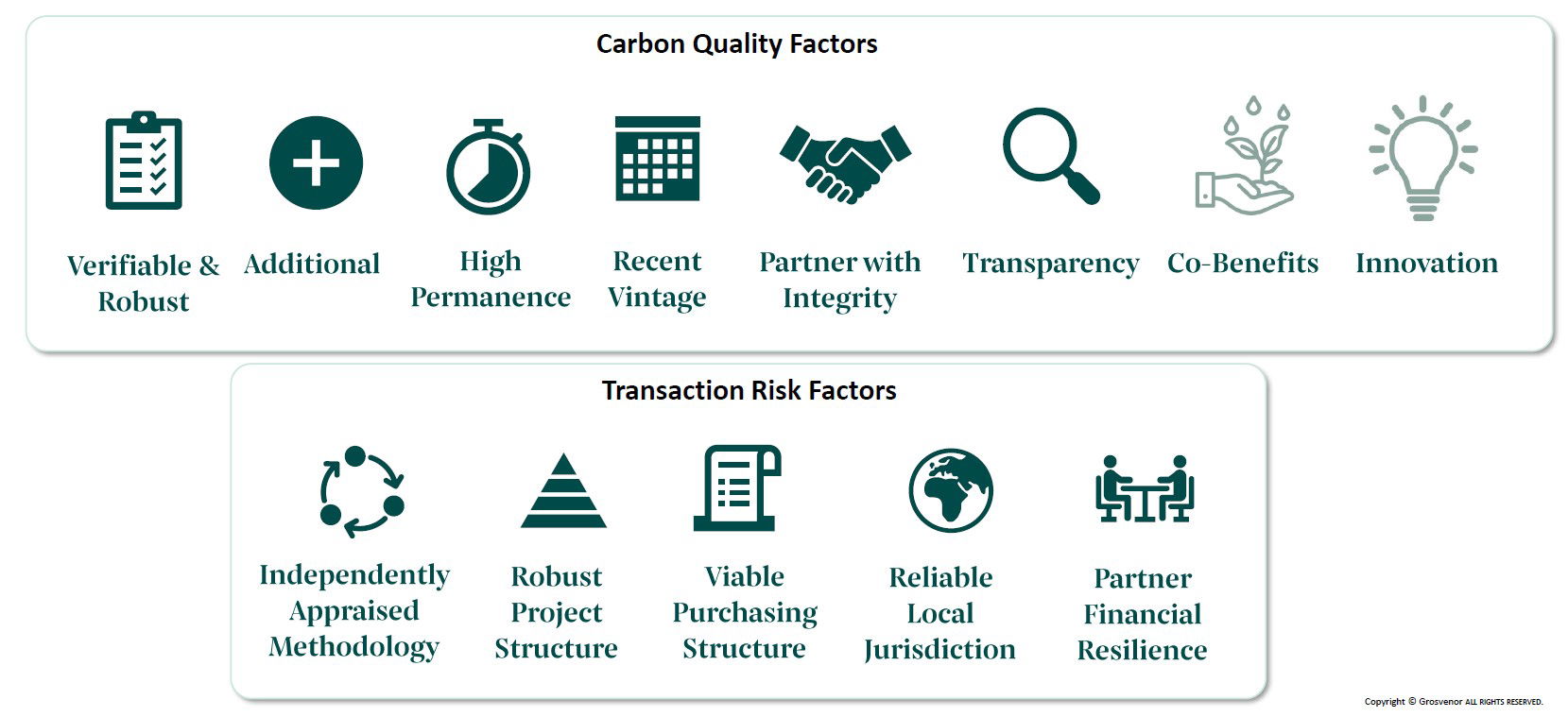

Projects should be evaluated on several fronts, including additionality (ensuring the project would not have occurred without the carbon financing), permanence (ensuring the carbon sequestration is long-lasting), and the risk of double counting (ensuring the carbon benefits of the project are not claimed by multiple entities).

Reducing your impact should always be the priority

To credibly use carbon credits, they should only be used as part of a wider net zero carbon commitment. Absolute emissions reductions should always be the priority. Grosvenor Property UK was the first European property company to have an approved long-term science based target, committing to a 90% absolute emissions reduction by 2040.

Through our efforts we are ahead of our pathway, having reduced our emissions across our entire carbon footprint by 26% since 2019. We are also committed to mitigating the emissions we cannot immediately reduce – and carbon credits are a way to do this and enhance our overall impact.

Our due diligence approach

In 2021, we made a commitment to mitigate the impact our residual carbon footprint from 2025 – acknowledging that while absolute emission reduction is our priority, the “why wait?” approach ensures we take responsibility for the carbon emissions we cannot immediately reduce as we work towards achieving our science based target. Early entry into the market has also enabled us to refine our process, become more discerning as a client and increase confidence in our investments.

Our due diligence process encompasses several stages of evaluation and scrutiny.

Key due diligence stages

Initial Assessment

Learning from the Oxford Offsetting Principles, we have developed our due diligence criteria. These assess the environmental and social quality of the project in delivering meaningful carbon and broader impact. They also assess the contractual, structural and partner related impacts of the project.

When we identify potential projects, we start by reviewing the project design documents and annual project reports against our due diligence criteria. Only projects that meet our thresholds against these criteria will progress for further consideration.

Background Checks & Ethical Business Practices

Ensuring the credibility and integrity of all parties involved is a critical step in our process. We conduct background checks on relevant parties, including developers and landowners, to mitigate risks related to corruption and other business ethics issues.

External Due Diligence & Standardised Assessment Metrics

Comprehensive external due diligence also complements our internal reviews. Our trusted legal counsel, who understands our strategy and values, prepares a detailed report that aligns with best practice and investigates a wide range of project specifics, such as land ownership, carbon rights, and additionality. This requires working with local counsel in the project jurisdiction to have confidence around product integrity. Metrics are rated and recommendations are made based on the findings.

Technical Review & Keeping Pace With New Technologies

For new and emerging carbon methodologies, we instruct a technical team to scrutinise processes and calculations to ensure they meet our selection criteria. This step is crucial for projects leveraging nascent technologies not yet typical to the VCM.

Due diligence criteria

Our experience

As businesses around the world continue to navigate their net zero journeys, the importance of due diligence cannot be overstated. Conducting thorough due diligence is essential to finding high-quality carbon credits that deliver on their promises. It is an investment in both environmental integrity and the credibility of the VCM.

There are many organisations such as brokers or ratings agencies, who are increasingly offering those services. But nothing beats conducting your own due diligence. By committing to rigorous evaluation and high standards, we can ensure that our efforts drive meaningful, positive change.

This has required us to maintain clarity of our selection criteria, effective contract negotiation and appropriate internal and external resourcing. Since 2021, we have sifted through over 200 potential projects, selected 30 for detailed screening, and found only four so far that met our requirements. For completed deals, the costs of conducting due diligence and completing the contracts are typically between 1-2% of the contract value for spot purchases and around 5% for investment projects. This is based on the scale of our credit take per project (20,000 – 50,000t).

For those buying larger contracts, of course the fee proportions would decrease. We regularly found that there is greater opportunity the larger the ticket size, both in terms of project availability and in negotiating best terms with the developer.

The process is a significant time and resource investment. However, it also has real benefits and has mitigated many risks for us. It has unearthed issues around land rights uncertainty, potential corruption risks, and additionality concerns. It has given us the confidence that we are securing high quality credits that deliver genuine environmental and social co-benefits, and are in line with our values overall.

We believe it will also save us money in the long run as prices for high quality credits inevitably increase.

Importantly, our approach supports the development of the market for high quality credits as well as helping us to avoid the reputational risk of being associated with low quality projects.

They may be polarising currently, but carbon credits are an inescapable part of the net zero equation. If we are serious about having a positive impact, we must be as serious about the quality of the credits we buy and projects we choose to support.

Our portfolio

In 2021, we published our Carbon Offset Strategy. This document supports our Net Zero Carbon Pathway, with a commitment to mitigating the emissions that cannot be immediately removed.

Diversification has always been central to our carbon credit strategy. As well as a range of projects, geographies and methodologies, we have invested in different markets to spread risk and fortify our long-term carbon ambitions. We have secured over 100,000t of credits from 4 projects, with a mix of spot purchases, forward purchasing, and investing in project origination.

Within our portfolio, we are proud to have been able to include a substantial number high quality UK based credits. This was achieved through early entry into the scheme via investment (rather than spot purchase). As a partner sharing in project risk, we can access a lower cost per credit.

Since 2021, our retirements have been from our 2 spot purchase projects.

Yaeda-Eyasi, Tanzania

Type: Deforestation prevention

Partner: Separately Purchased through both C Level, and MyClimate

Contract type: Spot purchase

Standard, type: Plan Vivo, REDD+

The Yaeda-Eyasi project works with hunter-gatherer Hadza and pastoralist Datooga communities in 12 villages in Northern Tanzania. The project protects more than 110,000 hectares of native dryland forest, strengthening land tenure, management capacity and local natural resource management. The scheme won the UN Development Programme (UNDP) Equator Award in 2019, where it was recognised “as an outstanding example of a local, nature-based solution to climate and sustainable development”. It has undergone numerous studies by universities including: an external four-year peer-reviewed study by the University of South Carolina looking at biodiversity enhancement; a Cambridge University study of land rights; and a University of Yale study of the benefits of the project. In 2023, the project also underwent a social return on investment study by Level.

CO2OL Tropical, Panama

Type: Reforestation and Agroforestry

Partner: Forliance

Contract type: Spot purchase

Standard, type: Gold Standard, Afforestation/Reforestation

CO2OL is planting a mix of native and commercial trees across 13,000 hectares of degraded land in Panama. The project created a novel financial model to encourage small holder farmers to diversify their practices and support ecosystem restoration. It provides sustainable timber production and cocoa cultivation, whilst also ensuring a diverse species mix for habitat restoration by protecting ¼ of the area as a dedicated nature reserve. The scheme was the first of its type to be accredited under the Gold Standard verification body, and has supported over 150 local jobs. The carbon benefits of the scheme have been evidenced in the multiple monitoring cycles of the scheme over its 27 years. It has planted over 7.5 million trees and provides safe habitats for 15 endangered animal species on the International Union for Conservation of Nature (IUCN)’s red list.

Anlo Wetlands, Ghana

Type: Mangrove restoration

Partner: Terraformation

Contract type: Forward purchase (2025-2029)

Standard, type: Verra, Tidal Wetland and Seagrass Restoration

Located in southern Ghana, this project restores lost mangrove ecosystems over 2,500 hectares using Verra (VCS) methodology VM0033. Mangroves are highly productive ecosystems, whilst providing storm protection to people and sensitive habitats. They are also critical to sustaining fish stocks, which is key to the local maritime economy. Annual monitoring through a mix of field measurements and remote sensing will quantify the carbon removed through the restored mangrove areas. The land and carbon rights have been formally contracted to the local community, and a carefully constructed revenue waterfall 60-65% of revenue flows into community trusts, ensuring proceeds are spent on local priorities. The project – which is seeking registration with Verra using the Climate, Community and Biodiversity (CCB) Standards – will create over 350 local jobs, over half of which will be held by women. As a ‘blue carbon’ project, it brings a very different ecosystem service, social impact and pricing dynamic compared to land-based projects.

Regenerate Outcomes, UK

Type: Regenerative farming

Partner: Regenerate Outcomes

Contract type: Investment

Standard, type: Verra, Improved agricultural land management

Regenerate Outcomes (RO) aims to support farmers in the UK to move to regenerative agriculture practices, improving soil health to sequester carbon from the atmosphere as well as increasing above-ground biomass and biodiversity. The scheme provides education, support, loans and funding to participating farms, which can be used to create new, resilient income streams for farmers as they generate carbon credits. Following a detailed soil carbon testing and baselining, farmers commit to adopt regenerative practices. Recurring soil carbon testing validates the carbon that is sequestered and the farmers get 67% of revenue generated by credit sales.